Brought to you by

Find the answers to this question and more in SIMA’s just-released Industry Impact Report.

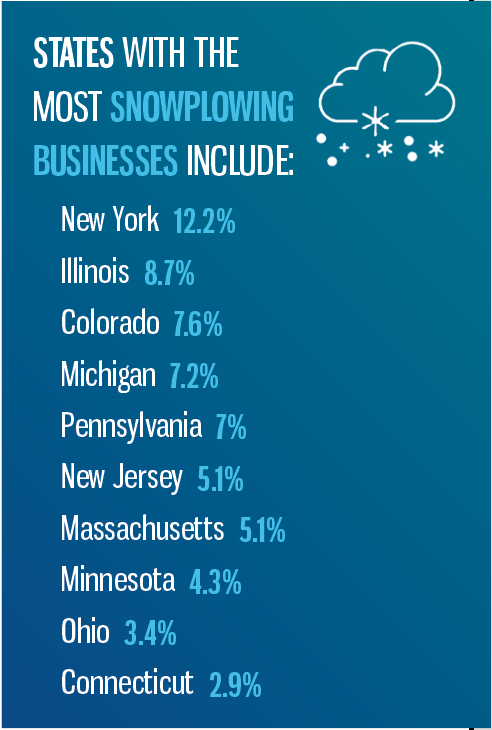

The Snow & Ice Management Association (SIMA) recently released an Industry Impact Report with important statistics for private-sector professional snow and ice operators. Here are some of the key findings for the U.S. market.

The U.S. private snow and ice management industry is estimated at $20.8 billion in revenues, spending $6.4 billion on labor and $5 billion on equipment. It comprises 88,200 businesses and 180,000 workers. The market is exceptionally fragmented. The top four largest operators control just 5% of the market revenue. The vast majority, four out of every five businesses, are sole proprietors.

The Providers

The typical snow and ice services provider…

- Has been in operation for at least 10 years.

- Generates revenue from snow and ice of $152,000. Runs a multi-line business including landscaping, earning $435,000. Snow and ice accounts for about 1/3 of its earnings.

- Serves 66 accounts, spanning 100 properties. Commercial clients comprise 60% of its business, residential 40%.

- Works 13-16 plowing events and 20-25 de-icing events per season.

- Has a one in six likelihood of facing a slip-and-fall claim each season. The average medical claim for a S&I-related incident is $33,000.

- Retains 93% of customers year over year.

Most providers offer several different services. Just 15% of operators are entirely or mostly dedicated to snow and ice management. On balance, the average operator earns 37% of their total revenue from snow and ice business. Over half of all snow and ice providers are lawn and landscape providers, who also offer snow and ice services.

The Market

Revenue has been growing 2.5% a year in the U.S. from 2016 (the last survey) to the present. (On par with U.S. GDP growth of 2% since 2016.)

The market is expected to continue to grow at 1.5% a year through 2026.

Commercial accounts (or Industrial) make up the greatest revenue segment at $7.1 billion and 35% of the market, up from 26% of the market in 2016. Desire for snow and ice services has increased as more major properties elect to out-source facilities management.

Residential accounts garner $5.9 billion and 29% of the market, a decrease from 34% of the market in 2016. This segment has declined somewhat, primarily due to lesser annual revenue from single-family housing in recent years.

Retail comprises $4.3 billion in revenues and 21% of the market, down from 27% in 2016. This segment is trending down recently, in part due to COVID-related declines in retail operations.

Medical brings in $1.7 billion at just 8% of the market, up from 7% in 2016. Institutional mimics these same figures exactly, bringing in $1.7 billion at 8% of the market, up from 7% in 2016.

The Business

Operations. Plowing accounts for half of all operations, though it has declined somewhat recently. It’s expected to grow again in upcoming years, as more large retailers choose to outsource snow removal. De-icing and anti-icing has grown slightly as a percent of revenue share. Snow clearing (as in sidewalk and doorway work) has also increased slightly. Residential and retail accounts generate greater revenue from parking lot and driveway plowing, while corporate and industrial accounts generate greater revenue from work such as de-icing, snow hauling, and sidewalk clearing.

Service Contracts. Most service contracts are variable price. Per push contracts comprise 24% of the market, per inch is 21%, time and materials is 16%, and per event is 14%. Seasonal contracts are used by 25% of respondents.

Tech. Technology is making the industry more efficient and productive. GPS is now mainstream, used by 70% of large (20+ employees) and 35% of smaller (six to 20 employees) operators. Telematics and IoT allow real-time location tracking, col-or-coded street maps to help prevent cover-age gaps, and Internet-connected property markers signal if a location still needs service. Tracker apps use autonomous vehicle location (AVL) to indicate snow removal progress. Electric or alternative fuel equipment is being purchased by 9% of respondents. What’s ahead? Droids and self-driving vehicles as well as heated roads. In fact, the town of Holland, MI has already built over 167 miles of heated road.

The Snow & Ice Management Association (SIMA) is a non-profit national trade association with a focus on training, events, and best practices related to snow plowing, ice management, and business management. The next Snow & Ice Symposium will be held June 13-16, 2023 in Hartford, CT. To view the full Industry Impact Report, visit sima.org.

Do you have a comment? Share your thoughts in the Comments section below, or send an e-mail to the Editor at cmenapace@groupc.com.

has released an Industry Impact Report with important statistics for snow and ice professionals.){kind=link}